You found an MSB for sale. The FINTRAC registration looks active, the price is fair, and the seller wants to close fast. Before you sign anything, you need to know what you are actually buying.

A money services business in Canada carries live federal obligations under the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA). Those obligations transfer with the business. If the seller ran a weak AML program, missed required transaction reports, or has a compliance examination sitting in their inbox, you inherit every bit of that on closing day.

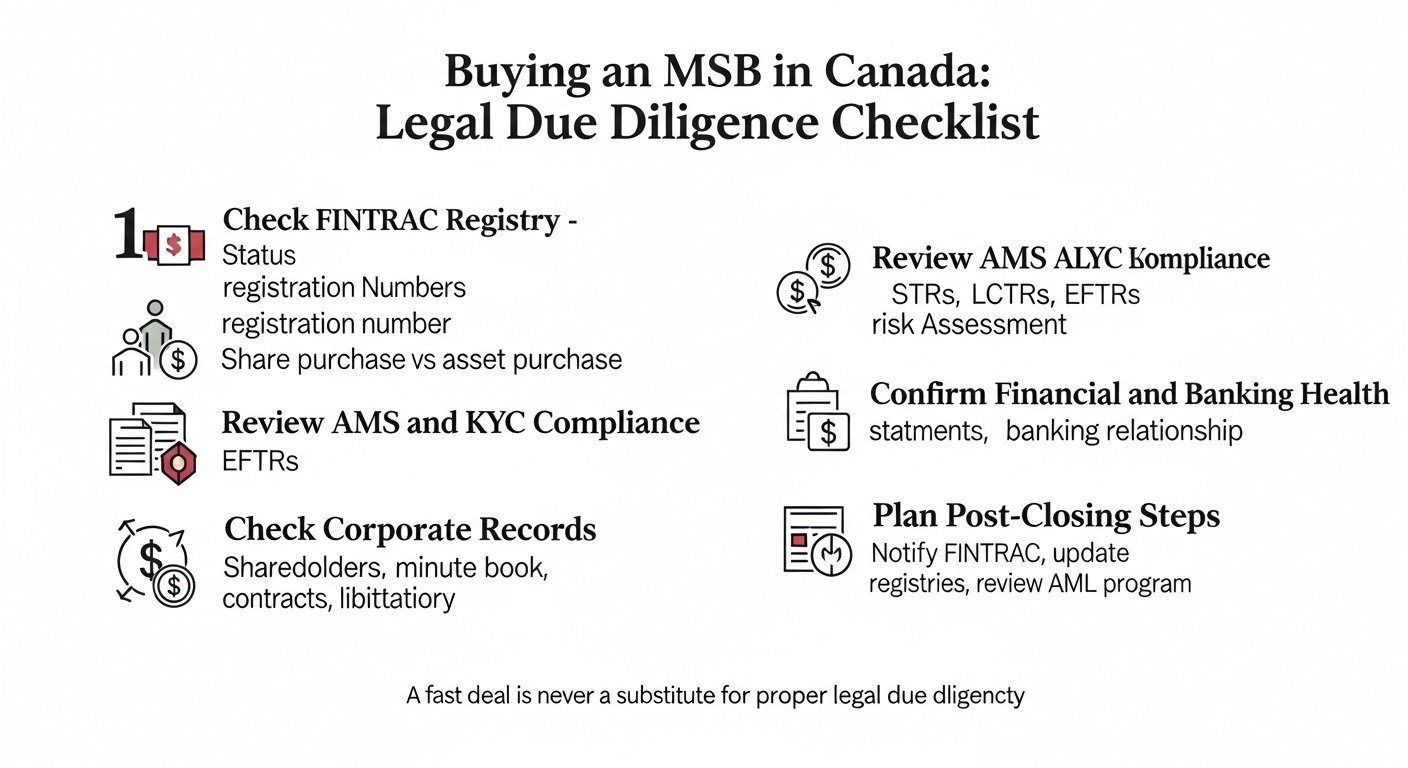

This guide covers what every buyer needs to check before committing to an MSB acquisition in Canada.

By the end, you will know:

- How to verify FINTRAC registration status before you sign a Letter of Intent

- Whether an asset purchase or share purchase fits your risk profile

- What a complete MSB legal due diligence checklist covers

- What post-closing steps are required under Canadian law

What Should You Check on FINTRAC Before Committing to a Purchase?

Start with the FINTRAC MSB Registry, a free public database, before you sign any agreement. This search takes minutes and tells you more than most sellers will volunteer upfront.

Four things to look for:

- Registration status: Should show “Registered.” A “Revoked” or “Expired” status signals prior non-compliance that stays on the record.

- Services listed: The categories on the registry must match what the business actually does. A gap here means the business may be operating outside its registered scope.

- MSB Registration Number: Confirm the number in the seller’s materials matches the public record exactly.

- Renewal date: FINTRAC registrations renew every two years. A registration expiring within the next 60 days with no renewal in progress is a warning sign.

After the registry search, ask the seller for their full compliance history, including any FINTRAC clarification requests received, examination findings, and prior renewal submissions. If the seller is reluctant to produce these documents, that hesitation is the answer.

One client came to us after discovering, three days before closing, that the MSB they were buying had an unanswered FINTRAC clarification request from eight months prior. That deal needed significant restructuring before it was safe to proceed. Running the registry search and asking the right questions at the start would have surfaced that issue in week one.

What Is the Difference Between an Asset Purchase and a Share Purchase for an MSB?

The structure of the deal determines whether you inherit the seller’s regulatory history or start clean. This decision matters more in MSB transactions than in almost any other business acquisition.

In a share purchase, you acquire the shares of the corporation that holds the FINTRAC registration. The registered entity does not change. You gain speed and continuity, as the banking relationship, compliance program, and registration number all stay in place. The trade-off is that you also take on every liability of that entity, including any AML failures, CRA exposure, or undisclosed enforcement actions that existed before you arrived.

In an asset purchase, you buy specific assets rather than the company itself. The FINTRAC registration does not transfer with assets, so you would need to register a new MSB or acquire a shelf MSB. You get a cleaner break from prior liabilities, but you lose the existing banking relationship and need time to rebuild the compliance infrastructure.

| Feature | Share Purchase | Asset Purchase |

|---|---|---|

| FINTRAC registration transfers | Yes, with notification | No, new registration required |

| Inherited liabilities | All prior liabilities | Limited to disclosed liabilities |

| Banking relationship | Typically retained | Must be re-established |

| Speed to operation | Faster | Slower |

| Best suited for | Clean, compliant MSBs | Cases where compliance history is unclear |

For a well-documented, actively compliant MSB, a share purchase with strong representations, warranties, and indemnity clauses can work well. Where the compliance record is thin or unclear, an asset purchase or a clean shelf MSB purchase may be the lower-risk path.

What Does a Complete Legal Due Diligence Checklist Cover for an MSB Acquisition?

MSB due diligence in Canada runs across three tracks simultaneously: regulatory and compliance review, corporate and legal review, and financial and operational review. A lawyer experienced in FINTRAC compliance due diligence will run all three at once.

Regulatory and Compliance Review

This is where the largest post-closing surprises come from, and where generalist lawyers most often cut corners.

- Confirm FINTRAC registration is current with no outstanding clarification requests

- Review the AML/KYC policy manual to confirm it meets current PCMLTFA standards

- Confirm a named compliance officer (CAMLO) is in place and properly documented

- Review at least two years of Suspicious Transaction Reports (STRs), Large Cash Transaction Reports (LCTRs), and Electronic Funds Transfer Reports (EFTRs)

- Check whether a FINTRAC compliance examination has occurred and review any findings

- Confirm the business’s risk assessment documentation is current and covers all active service lines

- Verify five-year recordkeeping obligations are being met VERIFY current retention period with legal counsel

- For virtual currency MSBs, confirm crypto AML policies are current with 2024 to 2025 FINTRAC guidance

- Check for any Administrative Monetary Penalties (AMPs) issued or pending

As of October 1, 2025, updated PCMLTFA regulations came into force requiring expanded criminal record checks for key personnel and new beneficial ownership transparency reporting tied to Corporations Canada’s federal registry. Any MSB you are buying should already be in compliance with these rules. VERIFY with current FINTRAC guidance at fintrac-canafe.canada.ca

Corporate and Legal Review

- Confirm the entity is in good standing under the Canada Business Corporations Act (CBCA) or the Ontario Business Corporations Act (OBCA), as applicable

- Review corporate minute books, shareholder registers, and all corporate resolutions

- Identify all shareholders owning 20% or more and confirm the ownership structure

- Review the shareholder agreement for any transfer restrictions or pre-emptive rights

- Search for pending litigation, regulatory orders, or outstanding judgments

- Review all material contracts, including banking agreements, agent agreements, and correspondent arrangements

- Review employment contracts and identify any key-person dependencies

Financial and Operational Review

- Review at least three years of financial statements and confirm transaction volume data

- Assess revenue by service line, including foreign exchange, remittances, virtual currency, and prepaid products

- Evaluate the banking relationship and check for any bank notices or at-risk account flags VERIFY banking status directly with the seller’s documentation

- Review operational costs, including ongoing compliance costs, which can be material for regulated MSBs

- Request CPA-reviewed financials where the transaction size warrants it

For a shelf MSB with no live operations, financial review is minimal. The FINTRAC status check and compliance program review become the primary focus.

If you are reviewing an MSB opportunity in Ontario or anywhere in Canada, Cloudhaus Law offers a free initial consultation to help you map out what the process involves before you make any commitments.

What Are the Biggest Legal Risks of Buying a Non-Compliant MSB?

Buyers who skip proper AML compliance MSB acquisition review take on three categories of risk.

Inherited regulatory liability.

Under a share purchase, you own the entity and its full history. If the prior owner failed to file required transaction reports or ran a deficient KYC program, FINTRAC can examine the business after closing and issue penalties for pre-closing failures. Administrative Monetary Penalties under the PCMLTFA can be material. VERIFY current AMP ranges with FINTRAC published schedules

Banking relationship loss.

Canadian banks routinely check the FINTRAC registry before onboarding MSB clients and are entitled to close accounts where compliance concerns exist. If the seller’s bank was not formally notified of the MSB ownership transfer in Canada, or if the bank has concerns about the change of control, the business may lose its account shortly after closing. Finding a new bank willing to service an MSB is one of the slowest parts of getting back to operational status.

Undisclosed enforcement.

FINTRAC does not publish all enforcement actions in real time. A seller may not volunteer information about an open examination or an unanswered clarification request. Your purchase agreement must include direct representations and warranties from the seller confirming that no enforcement actions, examinations, or pending compliance issues exist.

What Corporate Steps Are Required After an MSB Ownership Transfer in Canada?

Signing the purchase agreement is not the finish line. Several post-closing steps have fixed timelines under Canadian law.

- Notify FINTRAC within 30 days. VERIFY with current FINTRAC requirementsChanges to ownership, directors, compliance officers, or business location must be reported to FINTRAC within 30 days using the online change form in the MSB Registration System (MSBRS). FINTRAC will follow up through Canada Post Connect with further instructions.

- Update the corporate registry. Changes to directors, officers, or the registered address must be filed with the Ontario Business Registry for OBCA corporations, or with Corporations Canada for federal corporations under the CBCA.

- Review RPAA obligations. As of September 8, 2025, the Retail Payment Activities Act (RPAA) is in force and the Bank of Canada now supervises retail payment service providers. If the MSB also qualifies as a payment service provider under the RPAA, separate registration with the Bank of Canada may be required. VERIFY RPAA applicability with legal counsel based on the services offered

- Appoint or confirm the compliance officer. If the prior CAMLO is not continuing after closing, a new appointment must be documented and reported to FINTRAC.

- Update the AML/KYC compliance program. After any ownership change, the compliance program should be reviewed and updated to reflect new ownership, any service changes, and the incoming compliance officer’s approach. FINTRAC will review this document in any future examination.

Why Cloudhaus Law Is the Right Choice for Your MSB Acquisition

Cloudhaus Law, led by Irbaz Wahab, focuses exclusively on Business Law, Franchise Law, Restaurant Law, and MSB Law. MSB acquisitions are not a side practice. They are one of four areas the firm handles every week.

- Fixed-fee legal services: You know your exact cost before the file opens. No hourly billing and no surprises.

- Dual-licensed in Canada and the U.S.: Cross-border buyers and foreign MSB acquirers get legal support across both jurisdictions from a single lawyer.

- FINTRAC compliance built in: AML program review, KYC policy assessment, registration due diligence, and post-closing notifications are all handled within one file.

- 100% virtual service: Consultations, document review, and e-signing are done online. No travel and no delays.

- Free initial consultation: Book a call at no cost and with no commitment to understand what your acquisition actually involves.

- Proven track record: Cloudhaus Law has helped launch 100+ businesses, handled MSB files including FINTRAC registration and virtual currency compliance, and raised $22.5M in utility token market cap sales for fintech clients.

GTA and national service: Based in Richmond Hill, serving Toronto, Mississauga, North York, Burlington, Scarborough, and clients across Canada.

Frequently Asked Questions About Buying an MSB in Canada

What is an MSB in Canada and why does buying one require special legal due diligence?

An MSB is any business offering regulated financial services, such as currency exchange, fund transfers, virtual currency dealing, or money orders, under the PCMLTFA. Buying one requires special due diligence because FINTRAC registration obligations, AML compliance requirements, and reporting histories transfer with the business under a share purchase. You need to know what you are taking on before the deal closes.

Do I need to notify FINTRAC when I purchase an existing MSB?

Yes. Any change in ownership or key registration details must be reported to FINTRAC within 30 days using the online change form. VERIFY with current FINTRAC requirements. Failing to notify FINTRAC of a material change is a breach of the PCMLTFA.

What is the difference between an asset purchase and a share purchase for an MSB?

A share purchase transfers the registered entity, including its FINTRAC registration and compliance history. An asset purchase does not transfer the registration, so the buyer must register separately. Share purchases are faster but carry inherited liabilities. Asset purchases are cleaner on liability but slower to reach operational status.

What are the biggest risks of buying a non-compliant MSB?

The three main risks are inherited AML liability from prior compliance failures, loss of the banking relationship if the bank was not informed of the change of control, and exposure to FINTRAC penalties for pre-closing reporting gaps. Each is manageable with proper due diligence and well-drafted indemnities in the purchase agreement.

How long does the due diligence process take?

For a straightforward, compliant MSB, the process typically takes four to eight weeks once the seller provides complete documentation. More complex files, particularly those with compliance issues or unclear banking status, take longer. VERIFY with legal counsel based on the specific transaction.

Get Your MSB Acquisition Right from the Start

Buying an MSB in Canada without proper legal due diligence is one of the fastest ways to inherit a regulatory problem you did not create.

Run the FINTRAC registry search first. Choose your deal structure based on the compliance history, not just the price. Make sure your purchase agreement includes the representations and indemnities needed to protect you if something surfaces after closing.

Cloudhaus Law is ready to help you work through the full process, from the first registry search to final closing. Based in Richmond Hill and serving clients across the GTA and nationally. Call (647) 965-0516, email irbazwahab@cloudhauslaw.com, or book a free consultation at cloudhauslaw.com/contact.